The EU Banking Package

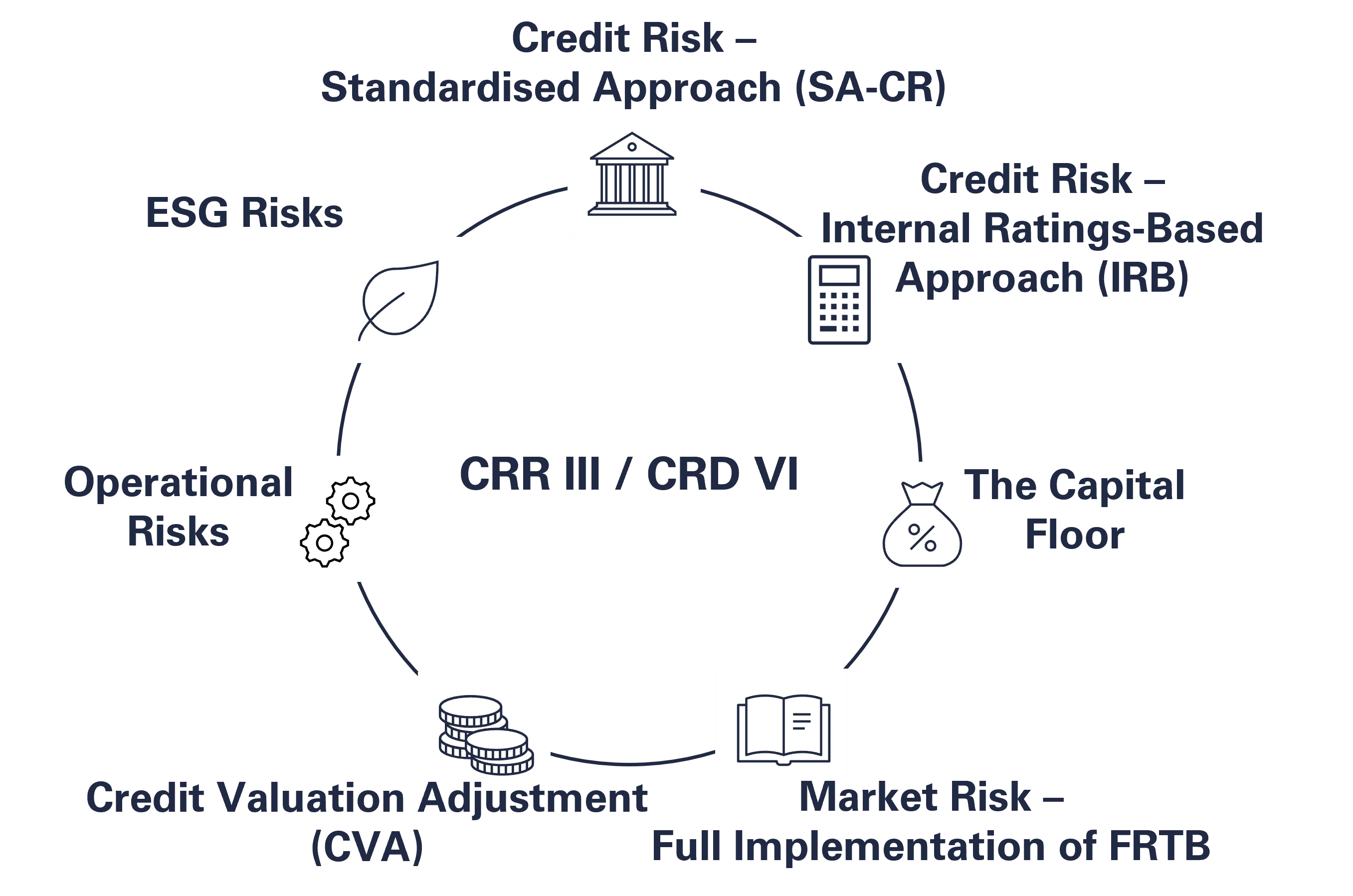

The entry into force of the new EU-launched the banking package is fast approaching. The changes to Regulation (EU) No 575/2013 in the form of CRR III and to Directive 2013/36/EU in the form of CRD VI are proposed to apply from 1 January 2025. The upcoming banking package will bring extensive changes, which means it is time to start preparing to ensure compliance with the new rules in a timely manner. The main changes in CRR III and CRD VI can be summarised in the seven areas illustrated in the figure below.

Credit Risk - Standardised Approach (SA-CR)

Credit Risk - Standardised Approach (SA-CR)

Credit Risk - Standardised Approach (SA-CR)

Credit Risk - Standardised Approach (SA-CR)Background

In order to reduce reliance on external classifications, increase risk sensitivity and promote comparability across credit institutions, changes to the current standardised approach for credit risk are introduced. These changes involve the introduction of more levels, categories and requirements, making the standardised approach more complex.

Exposure Value of Off-balance Sheet Items

Off-balance sheet exposures are adjusted to reflect the Basel III proposal, leading to higher risk sensitivity. The previous factor of 0 % is now replaced by a factor of 10 %. In addition, a factor of 40 % is introduced to further increase risk sensitivity. For a transitional period until 31 December 2029, credit institutions may continue to use the 0 % factor for unconditionally cancellable commitments. After that, the factor will increase annually by 2.5 % until it reaches the new level of 10 % on 1 January 2033. Credit institutions with significant off-balance sheet exposures, such as those via credit cards, could be significantly affected by this change, making it important to prepare.

Exposures to Institutions

Exposures to institutions are to be risk-rated using the existing External Credit Assessment Review Approach (ECRA), which is based on credit ratings from a nominated credit assessment institution (ECAI), or through the new Standardised Credit Rating Approach (SCRA). The SCRA requires credit institutions to categorise their institutional exposures that are not rated by an ECAI into three risk classes, based on both quantitative and qualitative criteria. With the introduction of the SCRA, the current possibility of using a sovereign credit rating to risk weight exposures to unrated institutions is discontinued.

Exposures Constituting Specialised Lending

The standardised approach for specialised lending introduces new exposure classes: project finance, asset finance and commodity finance. The European Commission considered that the standardised approach was not sufficiently detailed for specialised lending and has therefore made minor adjustments to increase the level of detail. The Commission has also decided to maintain the favourable treatment of high-quality infrastructure projects, a measure originally introduced in CRR II.

Retail Exposures

The definition of retail exposures is clarified in order to harmonise the application of risk weights in both the standardised and IRB approaches. In addition, credit institutions are permitted to apply a preferential risk weight of 45% to revolving retail exposures that meet certain payment or usage requirements, thereby improving their risk profile.

Exposures Secured by Real Estate

A reclassification of real estate secured exposures is being implemented to improve the level of detail on risks associated with different types of real estate transactions and loans. This new risk weight treatment maintains the differences between residential and commercial mortgage loans, but also introduces additional levels of detail regarding the type of financing and the stage of the property (either under construction or completed). Special treatment is given to properties whose instalments are dependent on the cash flow they generate (IPRE), as these loans are considered riskier than loans without the same cash flow dependence. In addition, the new risk weighting is based on the exposure-to-value (ETV) ratio, which means that a lower ETV ratio leads to a larger part of the loan receiving lower and more favourable risk weights, while a high ETV ratio has the opposite effect.

Credit Risk - Internal Ratings-Based Approach (IRB)

Credit Risk - Internal Ratings-Based Approach (IRB)

Credit Risk - Internal Ratings-Based Approach (IRB)

Credit Risk - Internal Ratings-Based Approach (IRB)The adjustments to the Internal Ratings-Based Approach (IRB) primarily affect institutions with exposures to large corporates, other credit institutions and other financial sector entities. These changes also apply to exposures to unrated entities and the use of Advanced IRB (A-IRB) models in relation to exposures to public sector entities and local and regional authorities. Furthermore, it is worth noting that the IRB approach is no longer authorised for the management of equity exposures.

The Capital Floor

The Capital Floor

The Capital FloorGeneral

The capital floor for credit risk has been the subject of extensive discussion, particularly in the Nordic countries where its impact is expected to be most significant. The capital floor aims to reduce the benefits credit institutions receive from using the IRB approach to credit risk. This floor will be phased in over a period of five years starting in 2025, starting at 50 % and gradually increasing to the final level of 72.5 % in 2030. The capital floor will then be equal to 72.5 % of risk-weighted assets calculated under the Standardised Approach for credit risk. This means that credit institutions using the IRB Approach will have to compare their capital requirements with those that would be required under the Standardised Approach. Due to historically low credit losses and a large share of low-risk assets in Swedish credit institutions, the capital floor is expected to affect Sweden and the other Nordic countries to a greater extent than the rest of Europe.

Exposures to Corporates Without an External Credit Assessment

A new transitional rule is introduced for credit institutions when calculating the capital floor for exposures to unrated entities. Under this rule, credit institutions may apply a risk weight of 65 % (instead of the normal risk of 100 %) to such firms when calculating the capital floor. This is applicable to both private and listed unrated firms, provided that their probability of default is less than 0.5 %. These transitional rules will apply until 2032.

Market Risk - Full Implementation of FRTB

Market Risk - Full Implementation of FRTB

Market Risk - Full Implementation of FRTBThe implementation of the Fundamental Review of the Trading Book (FRTB) was originally intended to be part of CRR II, but was postponed. Instead, only reporting requirements for the FRTB were introduced as part of CRR II.

Now, as part of CRR III, the full-scale implementation of the FRTB is taking place, integrating the Pillar I capital requirements for the FRTB. These changes aim to clarify and improve shortcomings in both the Standardised Approach and the IRB Approach, including clarifying the distinction between the banking book and the trading book. A significant change is the move to more risk-sensitive IRB approaches, replacing the current Value at Risk (VaR) risk measure with Expected Shortfall (ES). This aims to ensure that credit institutions can better capture more extreme market movements.

Credit Valuation Adjustment (CVA)

Credit Valuation Adjustment (CVA)

Credit Valuation Adjustment (CVA)The European Commission is implementing changes to the Credit Valuation Adjustment (CVA) requirements under the Basel III framework. These changes mean that the use of the IRB approach to calculate capital requirements for CVA risk is no longer authorised. Instead, three new approaches are introduced: the Standardised Approach (SA-CVA), the Basic Approach (BA-CVA) and also the Simplified Approach (AA-CVA). The SA-CVA requires specific approval as it is based on self-calculated CVA sensitivities to market risk. This also makes the standardised approach more risk-sensitive than before.

Operational Risks

Operational Risks

Operational Risks

Operational RisksFor operational risk, a lack of risk sensitivity in the current standardised approaches and a lack of comparability in the IRB approach across credit institutions have been identified, due to the freedom offered by the current Advanced Measurement Approach (AMA). In response, all existing methods for calculating capital requirements for operational risk have been replaced by a single, non-modelled approach that is now to be used by all credit institutions.

The new standardised approach introduced in Basel III is based on a Business Indicator Component (BIC), which divides the Business Indicator (BI) into three bands. However, the European Commission has chosen to exclude the loss indicator (ILM) in the CRR III approach. The BI is calculated using the formula

BI = ILDC + SC + FC

where ILDC is the interest, lease and dividend component, SC is the service component and FC is the financial component.

The aim of the new model is to harmonise and simplify the calculation of minimum own funds requirements for operational risk. By standardising the approach and using a uniform, non-model-based methodology, the aim is to create a more consistent and easier-to-understand system of capital requirements for operational risk for all credit institutions.

ESG Risks

ESG Risks

ESG RisksEnvironmental, social and governance (ESG) risks have been given a prominent role in the new banking package, notably through CRD VI. The European Central Bank (ECB) has recognised that if banks continue to transform at the current pace to promote a more sustainable financial industry, few will achieve the necessary objectives. To accelerate this transition, new definitions of ESG risks have been introduced and banks are now required to report their exposure to these risks. CRD VI includes new requirements that oblige credit institutions to integrate ESG factors into their strategies and processes for assessing internal capital requirements. This includes monitoring the credit institution's business model and strategy, which can be influenced by policies at both national and European level, in order to promote sustainable economies.

Executive Summary

The European Commission anticipates that the implementation of the new banking package will make the prudential rules for credit institutions more reliable and robust, which in turn will strengthen the EU banking sector and make it more resilient. The main objective of CRR III and CRD VI is to strengthen risk-based capital requirements without significantly increasing overall capital requirements. In addition, there is a greater emphasis on ESG risks in the prudential rules, which will play a significant role going forward. The overall changes are intended to foster European economic growth in the medium and long term. In addition, the aim is that future economic downturns will not be as deep as in the past and that the reforms will contribute to a stable recovery from the COVID-19 crisis.

Some of the changes introduced by CRR III and CRD VI are expected to have a greater impact on banking activities in Sweden compared with other European countries. A prominent example is the capital floor, which is likely to affect Swedish banks more due to the low risk weights that these banks apply in their internal credit risk models. It is important to note that Finansinspektionen has already introduced a mortgage floor of 25 % in Sweden, which means that it is not primarily mortgages that will be affected by the new European capital floor, but rather other types of lending, such as corporate loans.

Next Steps

As the entry into force of CRR III and CRD VI approaches, it is critical not to underestimate the time needed for implementation. If preparations have not already started, now is the time to start adapting to the upcoming changes. NFC has extensive experience in working with both CRR and CRD and can offer assistance to address the challenges posed by CRR III and CRD VI in a structured and efficient manner. Read more about our capital and liquidity adequacy services or contact us if you have any questions or need help analysing what the changes mean for you.