The New Rules for IRRBB

Updated on 2 May 2024 with links to the versions published in the Official Journal of the EU

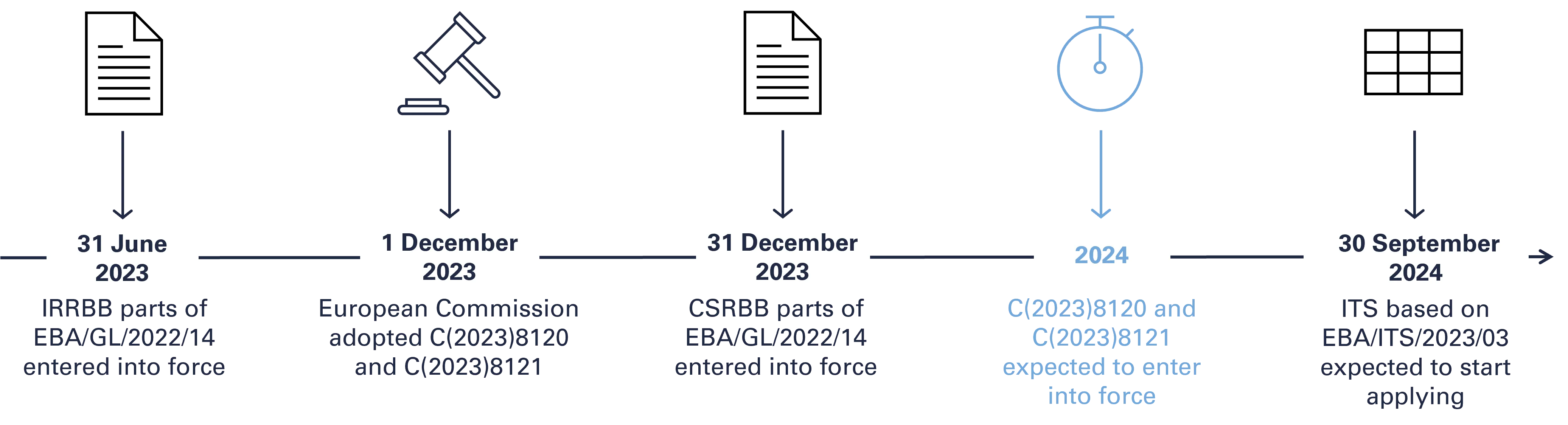

On 1 December 2023, the European Commission adopted the EBA's draft regulatory technical standards (RTS), C(2023)8121 (Published version: Commission Delegated Regulation (EU) 2024/857), which specifies standardised approaches for non-trading book interest rate risk (IRRBB), and the EBA proposal for the RTS, C(2023)8120 (Published version: Commission Delegated Regulation (EU) 2024/856), which specifies supervisory shock scenarios, common modelling assumptions and parametric assumptions to enable supervisory outlier tests (SOT) for the IRRBB.

The proposals were originally published on 20 October 2022 in a policy package together with the guidelines on IRRBB and credit spread risk arising from non-trading book activities (CSRBB), EBA/GL/2022/14, which you can read more about in our Article. The regulatory technical standards will enter into force 20 days after their publication in the Official Journal of the European Union (OJ). Against the background of the regulatory technical standards, the related reporting templates for the IRRBB were also developed in the draft Implementing Technical Standard (ITS), EBA/ITS/2023/03 (Published version: Commission Implementing Regulation (EU) 2024/855). This will lead to an increased reporting requirement when they become applicable by the reference date of 30 September 2024.

RTS Specifying Standardised Approaches for IRRBB

RTS Specifying Standardised Approaches for IRRBB

The RTS on standardised approaches describes standardised approaches to assess the risks arising from potential changes in interest rates affecting both the economic value of equity (EVE) and net interest income (NII) from non-trading book activities. The RTS describes how non-trading book interest rate sensitive items should be treated in the standardised approach (SA) for EVE and NII. Small and non-complex institutions may use a simplified standardised approach (S-SA) to reduce the modelling burden. Institutions may use internal measurement systems (IMS) for non-trading book interest rate risk, but if these do not fulfil the requirements for interest rate risk management, the local supervisor may require the application of SA or S-SA. The RTS covers the following areas for SA and S-SA respectively:

- Description of how to calculate EVE

- Description of how to calculate NII

RTS for Supervisory Outlier Test (SOT) for IRRBB

The regulatory technical standard on supervisory outlier tests describes how the EBA’s supervisory outlier tests (SOT) are to be calculated, by specifying common modelling assumptions and parametric assumptions to ensure consistent calculations across institutions. Consistent calculations generate results that are comparable and allow for effective monitoring against specific thresholds. The SOT is calculated for both EVE and NII, with EVE being monitored against the threshold of 15 % of T1 capital and NII against 5 % of T1 capital. The SOT is applied to detect outliers, and if thresholds are exceeded, the supervisor shall exercise its supervisory powers if deemed necessary. When calculating the SOT for EVE and NII, 6 and 2 standardised interest rate shock scenarios, respectively, are used to estimate sensitivity to adverse changes in interest rates. The RTS includes the following main areas:

- Description of how the interest rate shock scenarios are calculated

- Description of how to calculate changes in EVE

- Description of how to calculate changes in NII

- Description of a large decrease in NII

ITS for Supervisory Reporting on IRRBB

The ITS for supervisory reporting on IRRBB contains reporting templates and related instructions developed to enable the reporting of IRRBB outcomes and SOTs. The ITS includes a total of 11 reporting templates, which are divided into 5 categories:

- Evaluation of IRRBB: EVE/NII SOT and changes in market value

- Breakdown of sensitivity estimates

- Interest rate sensitive cash flows for repricing

- Relevant parameters

- Qualitative information

The reporting templates in each category are differentiated based on how the institutions are classified: ’large institutions’, ’small and non-complex institutions’, or ’other institutions’. Each institution concerned shall apply one reporting template from each category. The reporting templates containing quantitative information should be reported on a quarterly basis for each relevant currency, while the reporting template for qualitative information should be reported on an annual basis. Regardless of how institutions are classified, the new templates represent a significant increase in reporting requirements for the IRRBB.

Next Steps

NFC has extensive experience in both IRRBB and regulatory reporting. Our advice to our clients is to ensure that they comply with the new IRRBB requirements and at the same time start preparing to deal with the new more comprehensive IRRBB reporting requirements. Read more about our regulatory reporting services or contact us if you have any questions regarding the new EBA IRRBB and CSRBB guidelines, RTSs or upcoming reporting requirements.