Introduction

On 20 November 2026, a new Consumer Credit Act will come into force, significantly expanding the regulation of credit activities. The implementation of the EU's second Consumer Credit Directive introduces a general requirement to obtain authorisation for the provision of credit and credit intermediation services in relation to consumer credit agreements other than residential mortgages. The authorisation requirement applies regardless of whether lending is the company's main business or not. This means that a number of actors who today do not consider themselves lenders, for example, shops, car dealerships, and e-retailers offering instalment payments or other financing, may become so-called subsidiary lenders or credit intermediaries that require authorisation and are subject to supervision. For these companies, and for established lenders and credit intermediaries, the changes are extensive and require preparations well in advance of the application deadline in 2027.

Regulatory Framework

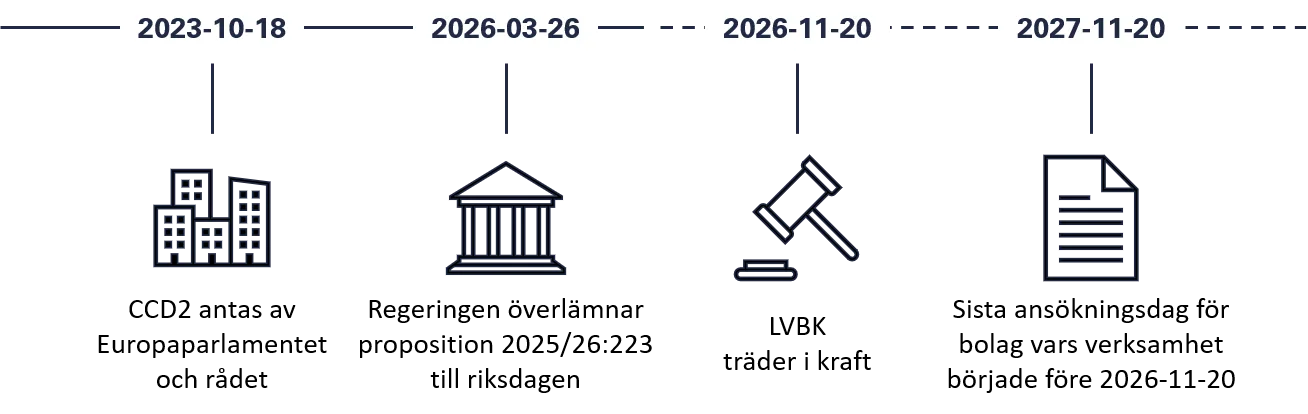

At EU level, the area is regulated by Directive (EU) 2023/2225 on credit agreements for consumers (CCD2), which repeals Directive 2008/48/EC. The Directive shall apply from 20 November 2026 and is essentially fully harmonising, which means that Member States may only depart from its provisions in specifically stated cases.

The Swedish implementation is set out in Government Bill 2025/26:223, A New Consumer Credit Act, which is based on Official Government Report (SOU) 2024:69 and provides for two concurrent reforms. First, the Consumer Credit Act (2010:1846) is replaced by a new Consumer Credit Act governing the relationship between creditors and consumers, including information requirements, creditworthiness assessments, the right of withdrawal, and caps on interest and charges. In addition, the Act on Mortgage Credit Business (2016:1024) is expanded to cover other forms of consumer credit and is renamed the Act on Mortgage Credit Business and Certain Other Consumer Credits (LVBK). The Consumer Credit Act regulates the conduct of creditors vis-à-vis consumers, whereas the LVBK regulates who may carry on the relevant credit activities

A New Authorisation Requirement

The principal regulatory change is the introduction of a general authorisation requirement for the provision of credit and credit intermediation services in relation to consumer credit other than residential mortgages, as regulated by the LVBK. As this requirement also applies where credit activities are carried on alongside another core business, it affects businesses such as retailers, car dealers and e-commerce operators that offer instalment payment arrangements or financing as part of their sales process. Depending on whether the business itself provides the credit or intermediates credit provided by another lender, it will be classified as either a subsidiary lender or a credit intermediary. Supervisory responsibility is divided between the Swedish Financial Supervisory Authority (Finansinspektionen) and the Swedish Consumer Agency (Konsumentverket), depending on the nature of the business and the type of credit offered.

Affected Companies

In practice, businesses fall into one of three categories:

- The first category comprises businesses that require authorisation from the Swedish Financial Supervisory Authority (Finansinspektionen) and are subject to its supervision. This is the general rule for subsidiary lenders and credit intermediaries. Applicants must be either Swedish limited liability companies (aktiebolag) or Swedish economic associations (ekonomiska föreningar). For subsidiary lenders, both ownership and management assessments are carried out, whereas this requirement does not apply to credit intermediaries only.

- The second category comprises businesses that are exempt from the Swedish Financial Supervisory Authority’s authorisation requirement and are instead subject to supervision by the Swedish Consumer Agency (Konsumentverket). This category includes smaller businesses whose activities consist either of providing interest-free credit in connection with the sale of their own goods or services, without any charges other than statutory late-payment fees, or solely of credit intermediation. The key concept is that of a “smaller business”, which under the Consumer Credit Act is defined as a business with fewer than 250 employees and either an annual turnover not exceeding EUR 50 million or a balance sheet total not exceeding EUR 43 million. Subsidiary lenders and credit intermediaries exceeding those thresholds therefore fall within the first category.

- The third category consists of credit institutions, payment institutions and electronic money institutions. These entities do not require any new authorisation, as they are already subject to supervision by the Swedish Financial Supervisory Authority by virtue of their existing authorisations.

New Regulatory Requirements

The new regulatory framework introduces two layers of requirements. The first applies only to businesses that are required to obtain authorisation and are subject to supervision by the Swedish Financial Supervisory Authority. The second applies to all businesses providing consumer credit or credit intermediation services, regardless of their size.

For businesses applying for authorisation from the Swedish Financial Supervisory Authority, assessments are carried out to ensure that the articles of association comply with applicable law, that the business can be expected to be conducted in a sound and compliant manner, that owners with qualifying holdings are suitable, and that members of the board of directors and the managing director possess sufficient knowledge and experience. In addition, information collected regarding consumers' personal and financial circumstances is subject to confidentiality obligations. Where businesses enter into outsourcing arrangements, including the outsourcing of operational functions, they remain responsible for the outsourced activities and must notify the Swedish Financial Supervisory Authority of the arrangement.

The ongoing conduct of business requirements under the LVBK apply to all businesses, regardless of whether they are subject to supervision by the Swedish Financial Supervisory Authority, and primarily cover five areas:

- Honesty and fair dealing. Businesses must conduct their activities honestly, fairly, transparently and professionally, with due regard to the interests of consumers.

- Knowledge and competence. Staff involved in providing or advising on consumer credit must possess adequate knowledge and competence, including knowledge of the relevant products and consumer protection legislation.

- Remuneration. Remuneration arrangements must not incentivise the number or volume of credits granted, and the remuneration of advisers must not be linked to sales targets.

- Advisory services. Advice must be based on the consumer’s financial circumstances and needs. Businesses must not present themselves as independent if they are, or have close links to, credit providers.

- Documentation. Credit decisions must be documented in a manner that enables the basis for the decision to be reviewed subsequently.

Regardless of whether a business is authorised, it remains ultimately responsible for ensuring that credit agreements comply with the substantive provisions of the Consumer Credit Act, including stricter creditworthiness assessments, caps on interest and charges, pre-contractual information requirements and the right of withdrawal. Supervision of these rules is exercised by the Swedish Financial Supervisory Authority in relation to businesses subject to its supervision, and by the Swedish Consumer Agency in relation to smaller businesses exempt from the authorisation requirement.

Implementation Timeline

The new rules enter into force on 20 November 2026, meaning that any activities subject to the authorisation requirement which are commenced after that date will require authorisation from the outset. However, operators already engaged in such activities at the time of entry into force may continue to operate without authorisation until 20 November 2027. Where an application is submitted by that date, the activity may continue until the application has been finally determined.

How NFC Can Support Your Business

Many companies that will become subsidiary lenders or credit intermediaries are not yet aware that they fall within scope, making an initial assessment important: does the company provide credit or carry out credit intermediation services, even indirectly, and if so, which category does the activity fall into? In group structures, several companies may require separate authorisations, for example a finance company acting as a lender and retailers acting as credit intermediaries. Even companies exempt from the authorisation requirement must establish procedures relating to knowledge and competence, remuneration arrangements and documentation.

NFC has extensive experience in financial regulation and in operationalising regulatory requirements into practical processes and internal governance documents. We can support businesses throughout the entire preparation process, from gap analysis and categorisation assessments through to authorisation applications, the development of internal policies and procedures, as well as adaptation to upcoming rules and regulations issued by the Swedish Financial Supervisory Authority. Read more about our licence application services or contact us if you wish to ensure that your business is prepared for the new requirements well in advance of the 2027 application deadline.