Tackling Key Issues in the EU Payment Services Market

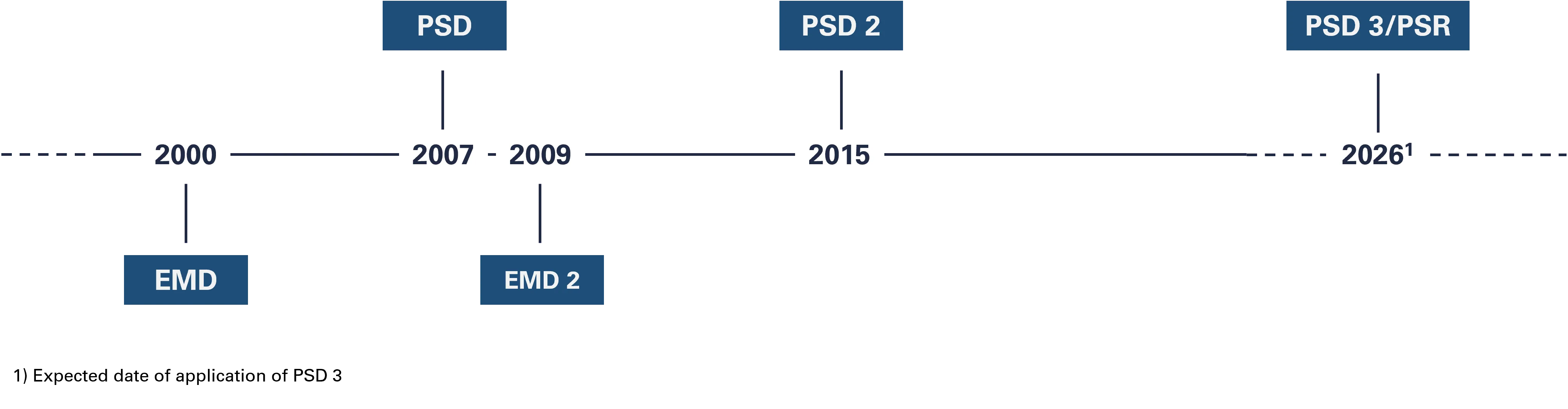

The European payment services market has been governed by four different regulatory frameworks since 2000, and in 2026 the two current frameworks PSD 2 and EMD 2 are proposed to be replaced by PSD 3 and PSR, integrating former electronic money institutions (EMIs) as a subset of payment institutions (PIs).

With the adoption of the first Payment Services Directive (PSD) in 2007, a legal framework was established to create an integrated payment services market in the EU. Due to the strong growth of Europe's payment services market between 2007 and 2018, the Directive (EU) 2015/2366 (PSD 2) was introduced on 1 May 2018, with subsequent revisions and further additions until 2019.

Ahead of the launch of the proposals for PSD 3 and PSR, the Regulatory Scrutiny Board (RSB) carried out an impact assessment which concluded that there are four key problems in the EU payment services market today, despite the successful implementation of PSD 2:

- Consumers are at risk of fraud and lack confidence in payments,

- The open banking sector is not functioning well,

- Regulators in EU Member States do not have the same powers and obligations,

- There is an uneven playing field between banks and other non-bank payment service providers.

The consequences of these problems include exposing consumers to fraud risks and limiting their access to reasonably priced payment services. In addition, banks providing open banking services face barriers in offering basic open banking services and lack of room for innovation. Due to the freedom that Member States have had in implementing the regulatory framework, specifically PSD 2, opportunities for regulatory arbitrage have arisen, giving operators in some Member States very large advantages in the market.

PSD 3 is being introduced with four specific objectives in mind to address and remedy the problems identified in the impact assessment:

- Strengthening user protection and trust in payments,

- Improve the competitiveness of open banking services,

- Improve enforcement and implementation in Member States,

- Improve (direct or indirect) access to payment systems and bank accounts for non-bank payment service providers.

What Are the Main Changes Compared to the Current Rules?

To strengthen user protection and trust in payments, several improvements are made to the application of strong customer authentication (SCA), for example when using virtual card payments. It also introduces an obligation for payment service providers to improve access to SCA for users who may have difficulties using the authentication methods, such as the elderly and people with disabilities. In addition, IBAN checks are extended to all payments, thereby reducing the incidence of fraud due to identity theft.

To improve the competitiveness of open banking services, account servicing payment service providers (ASPSPs) are required to set up a dedicated data access interface, known as ”infopanels”, to allow individual users to customise their access grants for open banking. PIs and EMIs will also benefit from fewer barriers to data access and greater access to the interfaces.

In order to better control the implementation of PSD 3 in the Member States, large parts of the PSD are moved to a directly applicable regulation, the PSR. It strengthens the provisions on sanctions and clarifies the wording, as well as integrating the authorisation schemes for PIs and EMIs. It also introduces a new authorisation regime affecting both PIs and EMIs, where they will have to apply for new authorisations as a PI. The existing authorisations will be extended by 30 months after the entry into force of PSD 3, and the new application for authorisation must be made within 24 months of the entry into force to give supervisors time to review the applications.

To address the difficulties experienced by non-bank payment service providers in opening accounts with banks, the rights to bank accounts for PIs are being strengthened and measures to increase the accessibility of payment systems are being introduced. To reduce the concentration risk of protected funds, new requirements are also imposed on PIs, requiring their protected funds to be held with several banks. In addition, PIs will have new possibilities to hold the protected funds with central banks.

What Are the Consequences for Those Applying the Payment Services Directive?

As part of the impact assessment, the implementation costs associated with PSD 3 were analysed. The results showed that the elements that will be introduced largely have no long-term impact on firms' costs. The costs that will be incurred are mostly one-off costs and will mainly affect account servicing payment service providers. In open banking, increased costs are offset by other savings, such as the removal of the requirement for a permanent back-up interface and the introduction of proportionality.

Banks whose liquidity consists largely of client funds from PIs and EMIs may be adversely affected by the possibility for these types of firms to open accounts with central banks with the intention of storing their funds there. If a bank's liquidity consists largely of this type of funds, it is therefore important to plan well in advance for the outflow of liquidity when the regulations come into force.

Another consequence for PIs and EMIs will be the requirement to apply for a new authorisation. No later than 24 months after the entry into force, all undertakings intending to continue their activities must apply for a new authorisation. The new application will have to be accompanied by a winding-up plan to support the orderly closure of the business in the event of failure. The major changes in PSD 3, the introduction of the PSR and, in particular, the requirements for new authorisation applications for payment and e-money institutions, make preparation for the new regulatory framework very important.

Next Steps

At NFC, we can help you tackle the upcoming challenges of PSD 3 and PSR in a structured and efficient way. We can also help you with new authorisation applications thanks to our experience with authorisation applications in connection with the introduction of PSD 2. Read more about our licence application services or contact us for more information.